Floor Plan Financing Bonus Depreciation

Kbkg Tax Insight Impact Of Bonus Depreciation For Companies With Floor Plan Financing Kbkg

2019 Bonus Depreciation Update For Auto Dealers Councilor Buchanan Mitchell Cbm

Bonus Depreciation Rules Favor Dealerships With Floor Plan Financing Interest 2019 Articles Resources Cla Cliftonlarsonallen

Product Page Skyline Homes Floor Plans Manufactured Homes Floor Plans Modular Home Plans

Thank You Factory Tour The Home Store Modular Home Floor Plans Two Story House Plans Pole Barn House Plans

2 Storey House Plans Floor Plan With Perspective New Nor Cape House Plans House Plans 2 Storey House Layout Plans

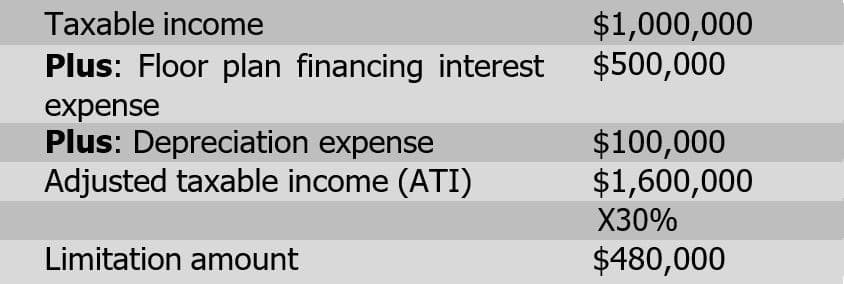

Specifically the 2019 proposed regulations address the following.

Floor plan financing bonus depreciation.

The Taylor House Plans First Floor Plan Ideas For Kitchen Into Great Room Floor Plans House Plans Garage Plans Detached

Plan 89988ah 3 Bed Craftsman Ranch With Open Concept Floor Plan Floor Plans Ranch Open Concept Floor Plans Ranch House Plans

Cypress Iii Floor Plan Bluestone Eastwood Homes Floor Plans How To Plan Richmond Homes

Plan 33117zr Net Zero Energy Saver House Plan Mediterranean House Plans House Plans Ranch House Plans

Plan 17801lv Stunning Open Floor Plan New House Plans Best House Plans Open Floor Plan

The Mcmillan Floor Plan Signature Collection Basement Floor Plans Rambler House Plans Basement House Plans

3 Bedroom Floor Plan C 9810 Hawks Homes Manufactured Modular Conway Little Rock Arkansas Bedroom Floor Plans Floor Plans 3 Bedroom Floor Plan

Ranch Style House Plan 3 Beds 2 Baths 1796 Sq Ft Plan 70 1243 Ranch Style House Plans Best House Plans Ranch House Plans

Plan 765011twn 5 Bed Beach Y House Plan With Two Upstairs Options Included House Plans Pier And Beam Foundation Architectural Design House Plans

Highland Homes Shennandoah Ii Floor Plans Highland Homes How To Plan

Plan 69554am 3 Bedroom Craftsman Ranch Home Plan Floor Plans Ranch Craftsman Ranch Craftsman House Plans

Laundry Craft Room Floor Plans Google Search Garage House Plans Bedroom Floor Plans Garage Floor Plans

Details Template Mobile Home Floor Plans Triple Wide Mobile Homes Modular Home Plans

Plan 022h 0022 House Plans Traditional House Plan Floor Plans

Plan 69270am European Luxury Plan With Angled Garage Garage Floor Plans Garage House Plans Country Style House Plans

Floorplan The Breeze Ii 34ssp28764ah Clayton Homes Of Athens Athens Tn House Floor Plans Clayton Homes Mobile Home Floor Plans

Lynnwood Gif 450 294 Floor Plans Ranch Raised Ranch Remodel Ranch House Plans

Country Style House Plan 2 Beds 2 Baths 1350 Sq Ft Plan 30 194 Country Style House Plans Floor Plan Sketch Floor Plan Design

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcqkeyoweol9qj1 Srfysmpcbicshchjhdme Mbk79qmjzva8jab Usqp Cau

Find Your Perfect Floor Plan Floor Plans Manufactured Homes Floor Plans House Floor Plans

The Keys Collection Hemingway Floor Plan In Solivita Kissimmee Fl Entry Foyer Kissimmee Fl Kissimmee

Residence 1 New Home Plan In Rancho Bella Vista Paloma One Storey House Floor Plans Dream House Plans

Cottage Style House Plan 75237 With 3 Bed 2 Bath 3 Car Garage Ranch Style House Plans Ranch House Plans Best House Plans

San Benito Floorplan 1848 Sq Ft Heritage Ranch Floor Plans Heritage House Plans

Source : pinterest.com